![]()

View Docs · Our Website · Join Our Newsletter · Getting Started

Blankly is an ecosystem for algotraders enabling anyone to build, monetize and scale their trading algorithms for stocks, crypto, futures or forex. The same code can be backtested, paper traded, sandbox tested and run live by simply changing a single line. Develop locally then deploy, iterate and share using the blankly platform.

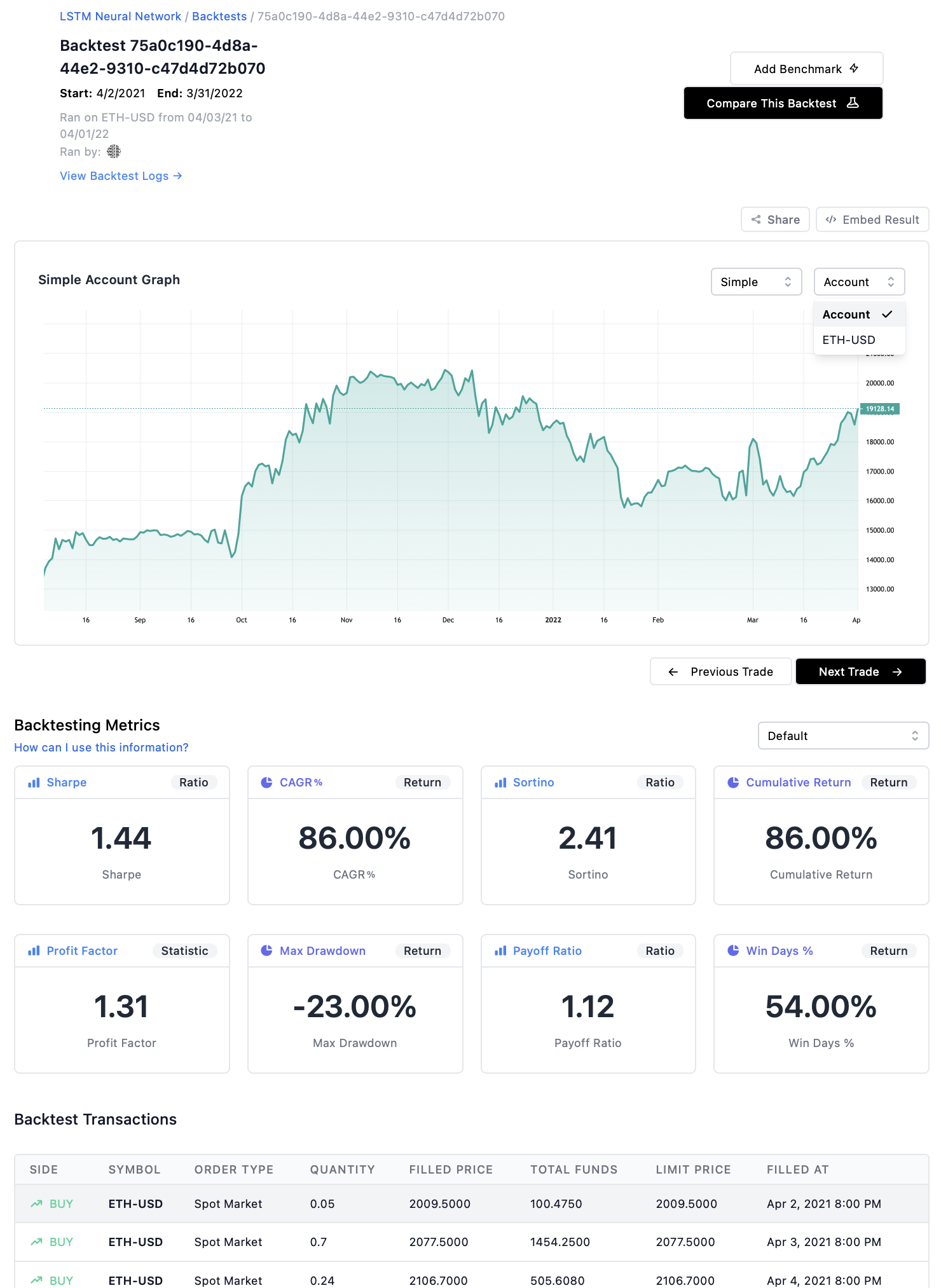

The blankly package is designed to be extremely precise in both simulation and live trading. The engineering considerations for highly accurate simulation are described here

Getting started is easy - just pip install blankly and blankly init.

Check out our website and our docs.

from blankly import Alpaca, CoinbasePro

stocks = Alpaca()

crypto = CoinbasePro()

futures = BinanceFutures()

# Easily perform the same actions across exchanges & asset types

stocks.interface.market_order('AAPL', 'buy', 1)

crypto.interface.market_order('BTC-USD', 'buy', 1)

# Full futures feature set

futures.interface.get_hedge_mode()import blankly

"""

This example shows how backtest over tweets

"""

class TwitterBot(blankly.Model):

def main(self, args):

while self.has_data:

self.backtester.value_account()

self.sleep('1h')

def event(self, type_: str, data: str):

# Now check if it's a tweet about Tesla

if 'tsla' in data.lower() or 'gme' in data.lower():

# Buy, sell or evaluate your portfolio

pass

if __name__ == "__main__":

exchange = blankly.Alpaca()

model = TwitterBot(exchange)

# Add the tweets json here

model.backtester.add_custom_events(blankly.data.JsonEventReader('./tweets.json'))

# Now add some underlying prices at 1 month

model.backtester.add_prices('TSLA', '1h', start_date='3/20/22', stop_date='4/15/22')

# Backtest or run live

print(model.backtest(args=None, initial_values={'USD': 10000}))Check out alternative data examples here

Seamlessly run your model live!

# Just turn this

strategy.backtest(to='1y')

# Into this

strategy.start()Dates, times, and scheduling adjust on the backend to make the experience instant.

- First install Blankly using

pip. Blankly is hosted on PyPi.

$ pip install blankly- Next, just run:

$ blankly initThis will initialize your working directory.

The command will create the files keys.json, settings.json, backtest.json, blankly.json and an example script called bot.py.

If you don't want to use our init command, you can find the same files in the examples folder under settings.json and keys_example.json

- From there, insert your API keys from your exchange into the generated

keys.jsonfile or take advantage of the CLI keys prompt.

More information can be found on our docs

The working directory format should have at least these files:

project/

|-bot.py

|-keys.json

|-settings.json

Make sure you're using a supported version of python. The module is currently tested on these versions:

- Python 3.7

- Python 3.8

- Python 3.9

- Python 3.10

For more info, and ways to do more advanced things, check out our getting started docs.

| Exchange | Live Trading | Websockets | Paper Trading | Backtesting |

|---|---|---|---|---|

| Coinbase Pro | 🟢 | 🟢 | 🟢 | 🟢 |

| Binance | 🟢 | 🟢 | 🟢 | 🟢 |

| Alpaca | 🟢 | 🟢 | 🟢 | 🟢 |

| OANDA | 🟢 | 🟢 | 🟢 | |

| FTX | 🟢 | 🟢 | 🟢 | 🟢 |

| KuCoin | 🟢 | 🟢 | 🟢 | 🟢 |

| Binance Futures | 🟢 | 🟢 | 🟢 | 🟢 |

| FTX Futures | 🟡 | 🟡 | 🟢 | 🟢 |

| Okx | 🟢 | 🟢 | 🟢 | 🟢 |

| Kraken | 🟡 | 🟡 | 🟡 | 🟡 |

| Keyless Backtesting | 🟢 | |||

| TD Ameritrade | 🔴 | 🔴 | 🔴 | 🔴 |

| Webull | 🔴 | 🔴 | 🔴 | 🔴 |

| Robinhood | 🔴 | 🔴 | 🔴 | 🔴 |

🟢 = working

🟡 = in development, some or most features are working

🔴 = planned but not yet in development

We have a pre-built cookbook examples that implement strategies such as RSI, MACD, and the Golden Cross found in our examples.

Other Info

https://blankly.substack.com/p/coming-soon

Please report any bugs or issues on the GitHub's Issues page.

Trading is risky. We are not responsible for losses incurred using this software, software fitness for any particular purpose, or responsibility for any issues or bugs. This is free software.

If you would like to support the project, pull requests are welcome.

Blankly is distributed under the LGPL License. See the LICENSE for more details.

New updates every day 💪.